In studying Strategic Management Accounting (SMA), it is useful to learn what the Management Accounting (MA) theorists, the MA professionals and the MA users say and actually do. To start with, SMA is accounting for strategic positioning or accounting for strategic management. It can also be stated that SMA provides accounting support to a company's management to formulate and implement business strategy so as to achieve sustainable

competitive advantage, and subsequently to monitor the effectiveness of its strategy.

Guilding, Cravens and Tayles (2000) maintain that conventional management accounting is mainly tactical, not strategic in orientation. These writers have identified a number of MA techniques that are considered as SMA techniques because these techniques possess one or more SMA characteristics, that is: marketing/ environmentally oriented, competitor-focused, long-term/ forward-looking oriented. Shank and Govindarajan (1993) state that SMA differ from conventional management accounting in terms of of their view of:

(a) what the most useful way to analyze costs

(b) what is the cost analysis objective

(c) how to try to understand cost behavior

Thus, to understand SMA, we need to understand (a) the subject of strategic management and then (b) what management accounting techniques are relevant to support strategic management practices in enterprises. (a) and (b) are closely related mainly in that a number of SMA techniques (or approaches) are firmly grounded on strategic management theories. For example, Shank and Govindarajan's (1993) strategic cost management is very much based on Michael Porter's value chain model. [Note: SMA techniques also adopt notions from other management disciplines, such as marketing, supply chain management, quality management, knowledge management, etc; thus, the subject is quite difficult to master, see

Ho (2011) .]

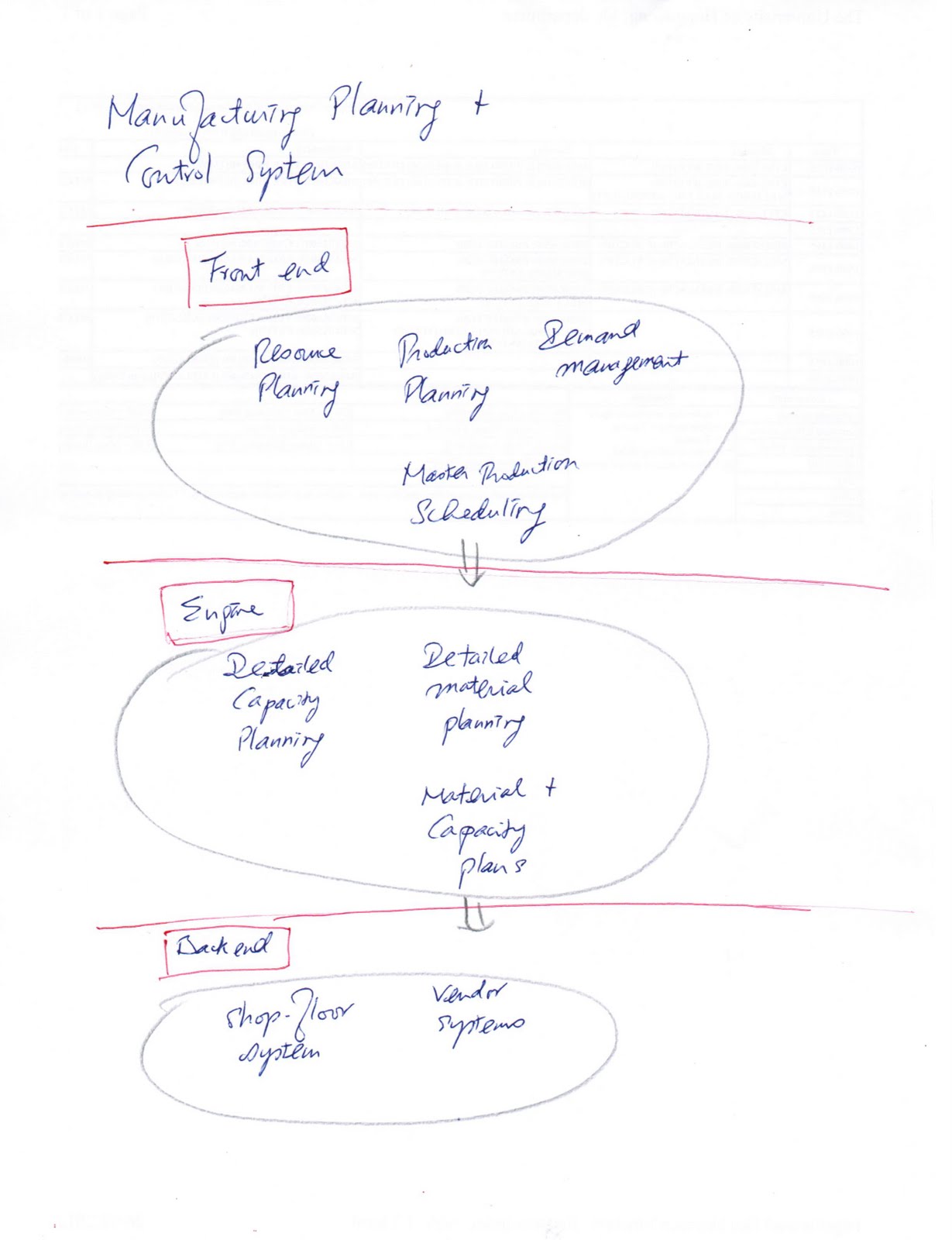

In this article, I am not prepared to elaborate what strategic management is; here, I want to emphasize that strategic management thinking is more external and future focused, as compared with operations management thinking. Thus, management accounting support for strategic management offers externally oriented accounting information such as customer accounting and competitor cost assessment as well as future oriented accounting information such as activity based costing (more concerned about cost behaviour in the long run) and balanced scorecard (with balanced performance assessment criteria for long term and short term considerations). In their discussion of strategic cost management, Shank and Govindarajan (1993) have a very compact way to relate SMA to strategic management, which is: a company can gain sustainable competitive advantage by (a) controlling strategic cost drivers better than competitors, and (b) reconfiguring its value chain appropriately. The following diagram depicts the relation of SMA with strategic management:

In general, we can classify SMA techniques as falling into the following categories (Cinquini and Andrea, 200): (i) competitor-oriented techniques, (ii) long-term/ future-oriented techniques, (iii) process/ activity oriented techniques, and (iv) customer-oriented techniques. Management Accountants make use of these SMA techniques to fulfill their business functions in scorekeeping, attention-directing and problem solving with regard to corporate strategic management. By doing so, they are then able to change their colleagues' perception of them as bean counters.

MA academics and professionals have been formulating and reviewing SMA techniques. One fundamental question in review of SMA techniques is: is a specific SMA techique really "strategic" in orientation, see for example CIMA (2007) paper on throughput accounting review. Besides, MA academics have been conducting empirical studies on actual SMA usage in business enterprises; they are aware that business enterprises may not practise SMA the ways the academics or the Management Accounting professional bodies expect even if ther SMA techniques are based on sound economic logic. The adoption of SMA techniques, like other forms of organizational innovation, can create organizational conflicts and tensions. This is because SMA practices are carrried out in enterprises that are human systems with rational-economic as well as non-rational-economic logic in operation. At other times, corporate management are interested in certain SMA information, e.g. competitor performance appraisal info., but their management accountants have difficulties to obtain and compile this information. It can also be the case that the management accountant of a specific company is not the best person (e.g. not senior enough) to champion an SMA implementation project in this enterprise. Besides, some of the SMA techniques have been mainly implemented by staffs other than management accountants, e.g. target cost management (Jack, 2008). On this topic of evaluation of SMA adoption, some SMA theorists have investigated the factors that affect the introduction of SMA in enterprises, such as Ma and Tayles (2009). I am sure evaluation of SMA practices will go on.

References

- CIMA (2007) "Theory of constraints and throughput accounting" Topic Gateway Series No. 26.

- Cinquini, L, and Andrea, T. (2007) "Is the adoption of Strategic Management Accounting techniques really "strategy-driven"? Evidence from a survey", MIPRA paper no. 11819. (url: http://mpra.ub.uni-muenchen.de/11819/)

- Comparative analysis of SMA: http://www.fachverlag.de/sbr/pdfarchive/einzelne_pdf/sbr_2006_july-234-258.pdf

- Guilding, C., Cravens, K.S. and Tayles, M. (2000) "An international comparison of strategic management accounting practices", Management Accounting Research 11, pp. 113-135.

- Jack, L. (2008) "Cost management discussion paper: From gate to plate: towards collaborative target cost management in agriculture and food", October, CIMA, UK.

- Ma, Y. and Tayles, M. (2009) "On the emergence of strategic management accounting: an institutional perpsective", Accounting and Business Research, 39(5), pp. 1-22.

- On Strategic Management Accounting (ACCA): http://www2.accaglobal.com/archive/sa_oldarticles/43981

- Shank, J.K. and Govindarajan, V. (1993) Strategic Cost Management, The Free Press.

- Strategic management accounting and control: http://astro.temple.edu/~banker/Accounting/StrategicManagementAccountingHandbookChapter.pdf

- Strategic Management Accounting techniques: http://josephho33.blogspot.com/2011/09/strategic-management-accounting.html

- Strategic management accounting and balanced scorecard: http://highered.mcgraw-hill.com/sites/dl/free/0077098595/74296/ch17.pdf

- Strategic management accounting and decision making: http://researchrepository.murdoch.edu.au/104/2/02Whole.pdf

- The strategic scorecards: http://hal.archives-ouvertes.fr/docs/00/58/47/72/PDF/SSRN.pdf

- Organizational configurations and strategic management accounting: http://webs2002.uab.es/dep-economia-empresa/documents/09-2.pdf

- Strategic management accounting and contingency framework articles: http://herkules.oulu.fi/isbn9789514287091/isbn9789514287091.pdf

- Strategic management accounting: lost in a name: http://www.sml.hw.ac.uk/documents/dp2010-aef05.pdf

{kind=link}